Pros and Cons of Creating Own Cryptocurrency in 2020

Cryptocurrencies and Blockchain technologies overall are becoming quite an essential part of modern life. There are hundreds of start-ups rising daily. For sure not of them are great, nor all of them are made by daydreamers. However, the matter of fact, this technology is on its steady growth. So let us today review, how to create a cryptocurrency and why it is important for your business.

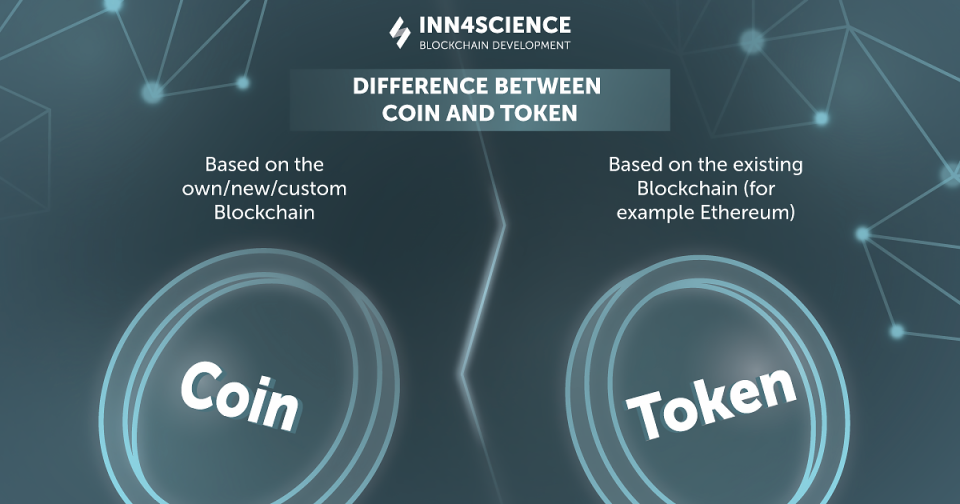

Feel the Difference Between a Coin and a Token

There are several ways of creating own cryptocurrency. We will discuss them further. Yet, before determining the way for the implementation, a crucial element is to choose what you are about to create. Сryptocurrencies are divided into two types: Coins and Tokens.

The interesting fact that the “name” of coin/token could be quite misleading and do not match reality. A cryptocurrency could have the word “coin” in its name while being itself a token.

So what is the difference between a Coin and a Token?

-

Coin

Coins in their core are the new modern form of money. Other ways of naming coins are altcoins or alternative cryptocurrency coins. And they for sure are very similar to traditional money, by having the same characteristics, they are: limited, reliable, portable, divisible and valuable. An indispensable condition to differentiate coin from the token that, a coin should be designed on a personal blockchain or at least being a hard fork of one (to have own independent transaction ledgers).

-

Token

Tokens, on the contrary, are assets that operate on the existing blockchain. Also, tokens are particularly bonded to one project (that has released the tokens). We can consider tokens as Frequent Flyer Miles.

Therefore, you actually can use both coins and tokens for paying over some certain products or services. However, while coins have an unlimited choice of use, you will be able to use tokens only at a particular “store”.

5 ways of creating a cryptocurrency

After you have made up your choice (what logic suits better, what type of currency to issue) we can move to the ways of creating your own crypto.

- To fork Bitcoin or another cryptocurrency.

Making a hard fork of the already existing currency means to take a popular coin (for example, Bitcoin) as a basis. And consequently, to implement into coin’s Blockchain some new functions or to fix bugs. The new coin will be automatically and equally distributed to those who already hold the coin, which was used as a fork basis.

- To create a cryptocurrency based on the so-called builder platform.

The most popular options are Ethereum, NEM, and Stellar. The real benefits here are the simplicity of issuance and popularity of the fundament platform.

- To create a token.

Tokens can serve as an indicator of property rights in real estate, business, etc. They also can be used for voting and polls processes.

Tokens can be divided into:

- Equity tokens that represent the company’s shares.

- Utility tokens that reflect value within the business model (on the platform, website, within a company, etc).

- Asset-backed tokens which are the digital obligations for real goods or services.

- To use frameworks for cryptocurrency development.

There are various frameworks, that can help to create own cryptocurrency. Those worth mentionings are Parity Substrate, Exonum, Hyperledger Fabric. Frameworks allow us to choose and combine different methods while designing new cryptocurrency.

- To build a completely new blockchain and cryptocurrency from scratch.

May seem like the best variant. However, it considers huge expenses due to the complexity of development. create a cryptocurrency exchange from a scratch implies solving challenges other blockchains can’t or bringing new methods to the market Thus, scratch development is a time-consuming option.

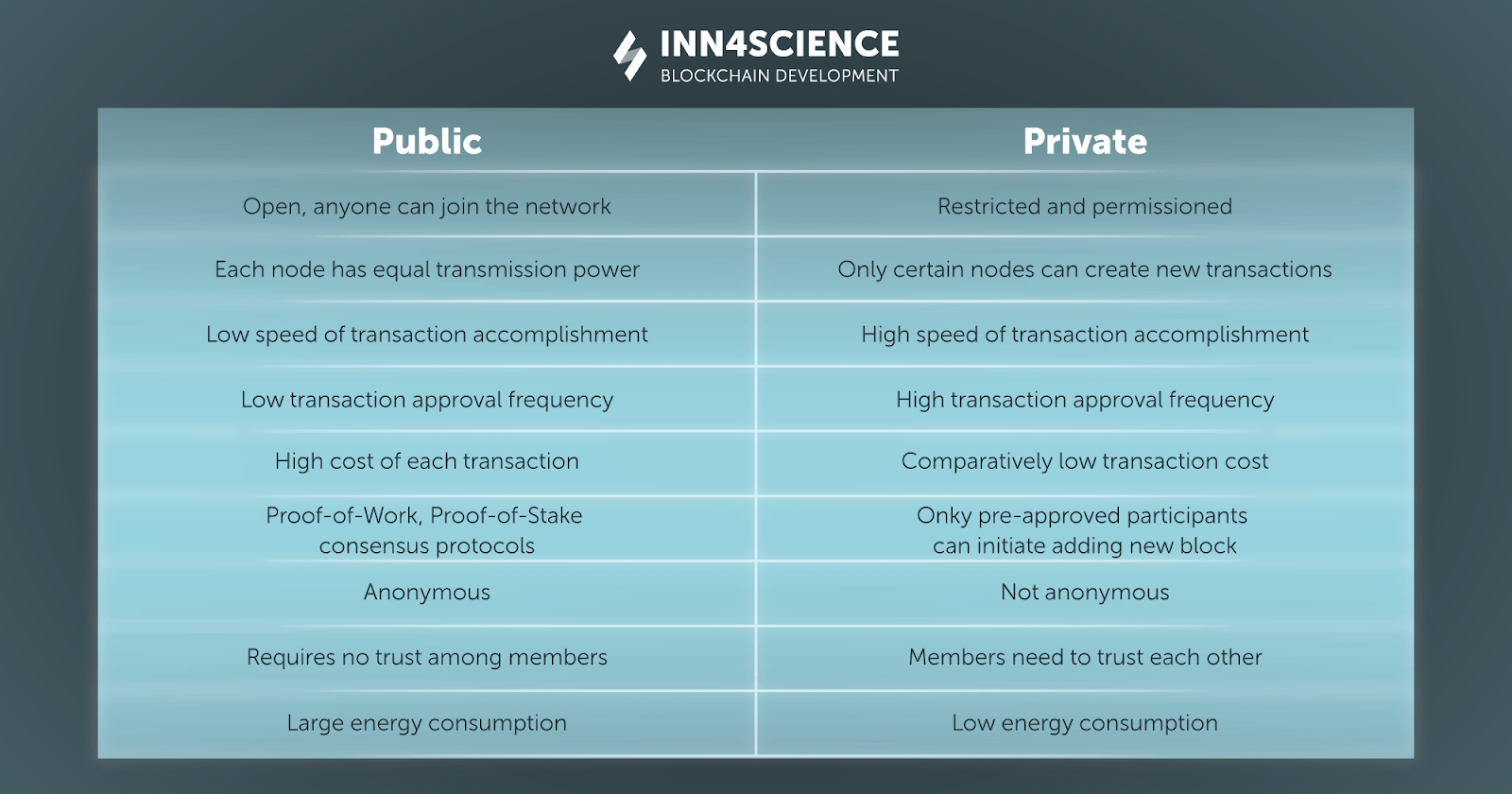

Choosing Blockchain

There are two different types of Blockchain: Private and Public. So what are their differences and which one to choose? Below you can find the table with a detailed description of both Blockchains’ principals of work. You can also check our article of how to create a cryptocurrency for more information and technical details.

Cons of creating own crypto

What may stop you from creating own cryptocurrency or what are the things to be considered before making such a decision.

- Potential users

This point is more related to start-ups than to already existing business. However, one should understand, that the real value of your currency is established when crypto has people using it. So the real problem for most enterprises is to attract potential customers.

- Criminal Uses

Actually, these works the same for cryptocurrencies as for traditional fiat money. You can create something legal, but you never know when it is used for illicit purposes.

- High Volatility

Keeping cryptocurrency at a stable price is quite challenging. The market price of any crypto changes faster than blinking with eyes.

Pros of creating own crypto

- Crypto is easy

When some can think that using crypto is difficult we want to ensure you, it’s super easy. Creating a transaction with crypto for your clients is much easier than sending a bank transfer.

- Cheap transactions

If you indent to use cryptocurrency as a mean of payment within your service(platform, company, etc.) you and your clients can save a lot on transaction fees. Unlike payment processors (like PayPal), crypto transactions have lower fees.

- Decentralization

As long as you give your money to a bank, they are no longer yours. Banks have full control of your account and funds there (for example, they can sign your account for monthly SMS subscription without prior notice and transfer the payment fee for this service directly from your account). A distinguish difference and advantage of cryptocurrency, that only owner of the crypto (person who has certain crypto on his account, not the creator of a cryptocurrency) can control the flow of the funds. Therefore you can be sure, that your money is safe and under your full control.

- Reduce fraud

Because all the transactions are written in Blockchain and cannot be changed in any way after the record. It won’t be any situation where one customer insists on sending the payment when it was not. And if going a little further, by using Blockchain technology and smart-contracts you can fully automate the receiving payment – providing product processes.

- Break barriers

Crypto is an international phenomenon. It brakes limits and barriers to process payments. Allowing you to easily accept payments globally without any restrictions.

Summary

An absolute trend for cryptocurrencies on the edge of 2020 is less investment, more use. As the market was overflown with ICO bubbles and needs a breath of fresh ideas. However, the technology itself has the future and constantly proves its usefulness. The question: “how to create a cryptocurrency” would not become irrelevant, as progress does not stand still, the new technologies do appear constantly. And we should ascertain the fact, that cryptocurrencies in their core can serve as a modern way of payment. Bringing simplicity, versatility, and efficiency to any type of business.

![]()