A few months ago, I read an article about a new transparent stablecoin with an inflation hedge, called Bustad coin. I wanted to know more about it and dug in deeper, got in touch with the team, and eventually wrote this article to tell the world about it.

In order to better understand the traits of Bustad I shall give a brief introduction to stablecoin basic mechanism before turning to some drawbacks of them. Once this is clear, it will be easy to understand

- What Bustad does better

- What is left to defined

- Where I see potential risks and weaknesses.

- Conclusion

Please note that this is no financial advice but rather of informational and educational character. I also want to point out that I have engaged myself in this initiative, as disclosed on my LinkedIn page.

Basic Stablecoin Mechanism

A stablecoin is usually minted with USDC, DAI or ETH. After the mint, the equivalent amount of a stablecoin is locked in a Multi-Party Computation (MPC) wallet or a multi-signature smart contract (“multi-sig” wallet) and secures (collateralizes) the value of the newly minted stablecoin.

All backed stablecoins1 use either “cryptocurrency” or fiat backing (for example USD), but there are also commodity-backed stablecoins. While the token backing happens on-chain, the fiat and commodity backing happens off-chain.

Once the stablecoin supply is in contraction, the issuer reduces the supply in order to keep the price relation stable to the reference asset.

Disadvantages

The disadvantages of securing a token with a stablecoin (which is then pegged to a fiat currency respectively) or with fiat currency backed directly lead to additional risks.

Inflation

Fiat currencies are terrible in value preservation as fiat currencies lose almost constantly in value. The US Dollar lost from its inception in 1635 until 2021 97,16%2 in value, and other currencies lost even more in much shorter timeframes. Also, in the shorter time horizon, inflation is not to be disregarded.

![]()

Buying Power of $100; Bureau of Labor Statistics, USA

Shady Businesses

The business models of the largest stablecoins are dominated by low-, or unregulated offshore destinations, lack transparency, and sufficient investor protection.

- All big three stablecoins3 claim to be backed by “fully reserved assets“ but not by the asset they actually are supposed to represent, the US Dollar itself. Tethers (Bitfinex) collateral contained commercial papers (CP) issued by Evergrande, China’s second-largest real estate developer, which is itself experiencing a major liquidity crisis. Just recently, on the 13. October 2022, Tether confirmed that they had stopped with this untrustworthy practice.4 Please note, the interest revenue received from CPs was not added to the “collateral” pool but seen as an extra income for the offshore firms!

- Tether is under investigation by multiple law enforcement agencies, including the U.S. Department of Justice and the FBI. The first fine came in October 2021, as the CFTC fined Bitfinex $42.4m for ‘untrue or misleading’ claims.5 It turned out that attestation was skewed, transferring $382m from its sister company, Bitfinex, hours before the accountants checked the numbers. In February 2022, Bitfinex reached an agreement over an $18.5m fine to settle a closely watched legal dispute with the New York attorney general’s office.6 New York’s top lawyer alleged that Bitfinex has used at least $700m from Tether’s cash reserves to cover up an $850 million loss. When these claims aired, the entire market shed about $10b in value.7 In other words, Binfinex has most probably lost this money meant for collateral because of speculation.

- It is not known where the offices of Tether are. iFinex, the mother entity, as well as Tether and Bitfinex are hidden organizations in a mesh of shell companies located in the British Virgin Islands, Hong Kong, Switzerland, and other jurisdictions. Circle has offices in the US, cooperates closely with regulators there and has legal entities in Wilmington and Ireland. Circle’s main flaw, besides centralization, is that they freeze USDC tokens that US regulators picked out (Tornado Cash dApp addresses).8

- The large stablecoins have published attestations for the collateral assets but have never allowed any audits to happen. Tether actually promised to deliver an audit in 2017, but we still wait for this to happen.

New Approach with (transparent) Inflation Hedge

Alf Gunnar Andersen saw these unsolved issues of inflation and transparency and thought about possibilities for solving this. The result was to safeguard as much collateral as possible by owning fractions (max 20%9) of housing properties, placing it on the Ethereum blockchain, and calling it Bustad coin.

According to the whitepaper, “real estate has proven itself as a good hedge against inflation. Private real estate tightly correlates with consumers’ purchasing power, which is the reason for inflation. This makes real estate a great store of value where your money retains its purchasing power.”10 As the collateral value grows, so does the value of the Bustad coin.

![]()

Alf Gunnar Andersen, CEO Horde AS and interim CEO Bustad Eiendom AS

The Bustad legal setup is as follows:

- The Bustad Association has legal ownership over Bustad Eiendom AS as a self-owned and non-profit organization.

- The Bustad Eiendom AS owns and manages the purchases and sales of the housing portfolio.

Tokenomics and Ownership:

- The Bustad coins (BUSC) are minted in interaction of an Ethereum smart contract and a non-custodial wallet. The Bustad multi-sig wallet receives the collateral while the non-custodial wallet receives the flatcoin. So far, around $40k BUSC has been minted.

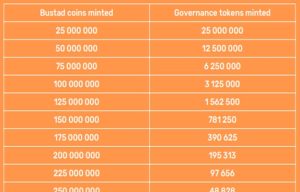

- The Eigar governance token: Until the first $25m BUSC are minted, the minter can also claim one Eigar token (EIG) for each minted BUSC. EIG is intended to give their holders influence in the Bustad Association that sets the policies. The ratio for the first 25 million tokens is 1:1. The next 25 million tokens have a ratio of 2 BUSC tokens for 1 EIG token (2:1). After that, halving every minted 25 million Bustad coins.

Source: Bustad Whitepaper

- 100.000.000 EIG have been pre-mined, 50% of them are dedicated for token minters, 25% are owned by Horde AS who provides office, infrastructure and does the development. The remaining 25% are dedicated to the team, the partners and the Bustad Association.

- The Bustad Eiendom AS will then purchase property on behalf of the Bustad Association and store the property data on-chain.

Why Start in Norway?

Norway’s high digitalization level makes it possible to connect the electronic National Public Ledger (“Grunnboken”) with all collateral on-chain on the Ethereum blockchain. This will provide full transparency and enables public audits as anyone can check and compare the value of the collateral with the price of the Bustad coin. The collateral value on Dune Analytics can be retrieved here. (Other countries might be rolled out later and potentially also new and different flatcoin with desired collateral exposure.)

Last but not least, Norway can be seen as an ideal starting point as it never had any extreme housing bubbles. The state, as well as the population, are among the richest in the world and Norway holds the silver medal of the Human Development Index (including a favorable Gini coefficient). Their sovereign wealth fund is the second largest pension fund in the world. This ranks Norway among the most attractive countries to start this endeavor!

Why not invest in Real Estate Companies directly?

Real Estate companies and securities are evaluated according to their estimated revenues in the future, which is a significant element of speculation.

Plus, these companies take up loans aiming to boost their returns which often leads to aggressive leverages. As a consequence, the price can get quite volatile and often unsustainable. Bustad cannot leverage its purchases and is priced based on the current market value of the properties owned, making it a much more stable asset and store of value.

Real estate companies also operate at higher costs compared to blockchain technology and its tokenized properties. Some may compare the Bustad coin to the traditional financial instruments of Exchange Traded Funds (ETF).

Left To be Defined

- As of today, EIG has not received any form of legal rights and its value is comprised of the anticipation of receiving influence to govern the Bustad Association as stated in the whitepaper. However, it lacks a detailed description on how the governance structure will look like. The priorities of the small team is now to focus on building a solution to purchase and sell property and get the legal prerequisites with the Norwegian Financial Authorities (Finanstilsynet) in place to start operations. How will the governance process look like for the Bustad Association and how much influence will be there?

- Securing price peg transition from USDC to collateral. Bustad needs to raise funds in order to be able to purchase housing assets. Therefore, an initial price of 1:1 to a dollar was determined. In the mid-term the price shall orientate on the value of its backing (otherwise there is simply no inflation hedge). In case the price rises significantly above $1, arbitrageurs will step in, mint BUSC and sell them on the decentralized exchange. Therefore, the minting price determination process should be changed and pegged to the collateral value price.

- Avoid market inefficiencies. The price is determined by the market and moves around $1. Bustad’s backing value is 11% above the token price since a few weeks. According to the whitepaper, Bustad Eiendom AS will counterbalance market inefficiencies (overhangs of demand or supply) according to liquidity of the collateral pool. My suggestion would be to define a transparent policy for this soft market making. Investors should feel safe to rely on a rather stable BUSC price that reflects approximately the collateral value. As an idea, I would see a corridor of 7-15% around collateral value. Arbitrageurs are then encouraged to do the job with Bustad as liquidity provider of last resort.

What are potential Risks and Weaknesses?

- The Bustad project is in its humble beginnings, and failure rates for early-state projects are high. However, the upside potential of the governance token reflects a fair risk-reward ratio for investors. Alf Gunnar, the main driver of this project, has an impressive track record of accomplishing missions as we can see with the Horde App. It is one of the most downloaded Financial Advisory apps in Norway.

- Norwegian regulators could delay or as a worst-case scenario even kill this initiative. Bustad has entered unknown territory in Norway. So far, the Norwegian Financial Authorities (Finanstilsynet) are seen as cooperative. Again, Alf Gunnar is a profound asset here as he is the founder and chairman of Fintech Norway (FTN). FTN is Norway’s largest lobby organization for fintechs in Norway and an important spearhead for Open Banking. Bustad has also qualified help from the PWC legal team around Daniel Næsse. Will the legal framework be sufficient for a stablecoin in Norway?

- In case Bustad is “too successful”, one of the big stablecoin competitors could copy Bustad’s strategy and try to corner Bustad. The earlier Bustad will be challenged, the higher the chances to corner successfully. However, this also correlates negatively with the probability of success, implying that the contender will disrupt their own extraordinarily profitable niche! In my eyes, this would include becoming fully on-chain and audited, which seems to be a very unlikely outcome.

- There are not enough real estate sellers for Bustad. In this case, the collateral will consist mainly of stablecoins (losing the important inflation hedge feature). Bustad Eiendom AS has a waiting list of interested homeowners to be worked off first. In the long run, much will depend on a fair policy to purchase and sell the property. The policy will be determined by the Bustad Association and eventually the holders of the Eigar token.

- Sufficient BUSC must be minted upfront in order to have the pool for a diversified property portfolio.

- The current bear market surely does not encourage investments in the blockchain space.

- International TradFi investors might not be very interested in gaining exposure to the Norwegian real estate market through blockchain technology.

The probability for this is significant as well-established projects with solid figures also experience reduced growth. Bustad is planning a few initiatives and campaigns. So far, there are plans to increase the traction via:

- Airdrops of the governance token Eigar,

- Bootstrap campaigns where the investors of BUSC as well as Bustad’s liquidity pools will receive Eigar tokens as rewards.

- The “cross-selling” capabilities to attract the Horde app users should not be underestimated, as the team is well-known and respected in Norway.

- The minting of larger sums works fine, but how to get out of a larger BUSC position at the moment? BUSC is traded on Uniswap in a V3 liquidity pool, however the pool is still small with a total value locked around $40k.

- Since this is a new token, the decentralized finance investment possibilities are limited to liquidity pools at the moment. The future will bring more utility for BUSC and for EIG.

Conclusion

Despite significant risks and drawbacks, stablecoins have shown impressive growth, and their apparent advantages prevail, including even Tether. Visa and Mastercard are working on solutions to integrate crypto payments. We can assume that we have just seen the beginning of the stablecoin growth.

![]()

Source: https://www.theblock.co/data/decentralized-finance/stablecoins

The market share of the largest stablecoins hasn’t changed much in recent years. It wouldn’t be very realistic to believe that Bustad could enter the Top 5 stablecoin list anytime soon.

Coinmarketcap.com lists over 130 stablecoins. Many, if not most of them are copycats with slight differences if all. Relatively few are of interest but probably more from an experimental point of view. This is where Bustad is different, as it doesn’t seem experimental but combines best practice of blockchain technology with best practice of a traditional (conservative) asset class. Most stablecoins have only one –use-case, the sometimes quite shaky short-term stability through a dollar peg. Bustad has, besides its different stability approach, also additional use cases:

- The tokenization of a traditional asset class

- A long-term value investment with property exposure

- Full transparency on the collateral

When there are known people and legal entities involved it gives me the comforting feeling of real ‘skin in the game’, and this can only be topped by a well-known and respected team.

The Bustad coin is still in a very early stage of development and so is the whole tokenization industry. The majority of holders of larger stablecoin positions are rather institutional funds and tech savvy individuals leveraging their harvest from decentralized finance.

The Eigar governance token is a tempting free-to-claim incentive for BUSC holders that could likely turn out to receive substantial value and upside potential over time.

Bustad is of interest for these investors:

- A long-term investor with demand for property exposure and most probably also decentralized finance strategies in the future.

- A mid-term-oriented investor who purchases Bustad coin in order to be eligible to claim the Eigar governance token which might be the token with the highest price increase potential.

- A safety-oriented Investor that doesn’t trust fiat denomination but physical assets on the blockchain. (However, may wait with minting BUSC until the first property has been bought.)

I am very excited about the mission, the vision, the team, and the founder. I believe that Bustad products can fill an important gap in the long run. The project state is very early! Maybe too early to call with certainty, but so is the risk/reward ratio.

The future looks bright, but all readers will eventually need to do their own research as well and let me know to which conclusions you have come.

Don’t trust, verify!

![]()

Subscribe to my free newsletter here: https://trustlessinvestor.substack.com/?utm_source=homepage_recommendations&utm_campaign=1195350

You guessed it, there are also unbacked stablecoins.

Bureau of Labor Statistic, USA; https://www.in2013dollars.com/us/inflation/1635?amount=100

Tether, Circle USD and Binance USD

Tether News; https://tether.to/en/tether-slashes-commercial-paper-to-zero

https://www.cnbc.com/2021/02/23/tether-bitfinex-reach-settlement-with-new-york-attorney-general.html

https://www.cnbc.com/2019/04/26/cryptocurrency-bitcoin-price-falls-on-ny-ag-bitfinex-probe.html

The maximum 20% stake shall secure responsible property ownership.

The ratio for the first 25 million tokens is 1:1. The next 25 million tokens have a ratio of 2 BUSC tokens for 1 EIG token (2:1). After that, halving every minted 25 million Bustad coins. A favorable bootstrapping mechanism in my eyes.

![]()